Quick Answer: Freezing your child’s credit makes sense for high-risk situations like foster care, divorced families with estranged relatives, or existing suspicious SSN requests – but low-risk newborns in stable families may be better served by annual monitoring and strong SSN protection practices.

Every parenting blog tells you the same thing: freeze your child’s credit the moment they’re born. They paint it as simple, free, and foolproof protection. The reality? Far more complicated.

Child identity theft affects 3% of all identity theft reports in the first half of 2024 according to Federal Trade Commission data, up from 2% annually between 2021 and 2023. While concerning, freezing credit isn’t the universal solution experts claim. The process takes hours of documentation across three bureaus, creates unexpected complications when teens need to build credit, and provides zero protection against medical identity theft or tax fraud.

Research shows 75% of child identity theft cases involve someone the child or family knows – a parent, guardian, or close relative with easy access to sensitive information. The conventional wisdom assumes all children face equal risk, but that’s dangerously misleading.

Table of Contents

- Key Takeaways

- Does Your Child Actually Need a Credit Freeze?

- Who Should Freeze Child Credit Immediately

- Who Probably Doesn’t Need Child Credit Freeze

- The Freeze Process: What Actually Happens

- Better Alternatives for Low-Risk Families

- If Your Child Already Has a Credit File

- When to Freeze vs. Monitor

- Making the Right Choice

- Frequently Asked Questions

- Sources

Key Takeaways

- One in 50 children falls victim to identity theft annually, with Javelin Strategy & Research reporting 915,000 cases in 2022 versus only 21,420 FTC reports for victims under 19.

- Over 600,000 children in U.S. foster care face extreme identity theft vulnerability because their information can be accessed by noncustodial family members, foster parents, and social services personnel.

- Credit freezes require mailing physical documentation to all three bureaus separately, taking 2-4 weeks versus instant online freezes for adults.

- Teens aged 16-17 who need to build credit through authorized user status must have freezes lifted – which parents often forget until application denials occur.

- Annual credit checks combined with strong SSN protection provide adequate security for most low-risk families without freeze complications.

- Explore Batten’s identity protection collection for family monitoring services that detect suspicious activity across credit bureaus and dark web exposure.

Does Your Child Actually Need a Credit Freeze?

Before spending hours gathering documents and mailing letters to credit bureaus, answer this: what specific threat are you protecting against? A credit freeze prevents one thing – unauthorized credit applications. It doesn’t stop medical identity theft, tax fraud, or family member fraud.

Child Credit Freeze Downsides Nobody Mentions

- Medical Identity Theft Happens Anyway: Medical identity theft accounts for 2 million fraud cases. Hospitals don’t check credit reports before providing emergency care.

- Tax Fraud Remains Possible: Identity thieves can file false tax returns using your child’s SSN. The IRS doesn’t check credit reports when processing returns.

- Teen Credit Building Problems: Adding teens as authorized users at age 16-17 to build credit history requires unfreezing all three bureaus first – something parents discover only when applications are denied.

- False Security: Parents think they’ve locked down identity completely, but freezes miss employment fraud, government benefit fraud, and utility account fraud.

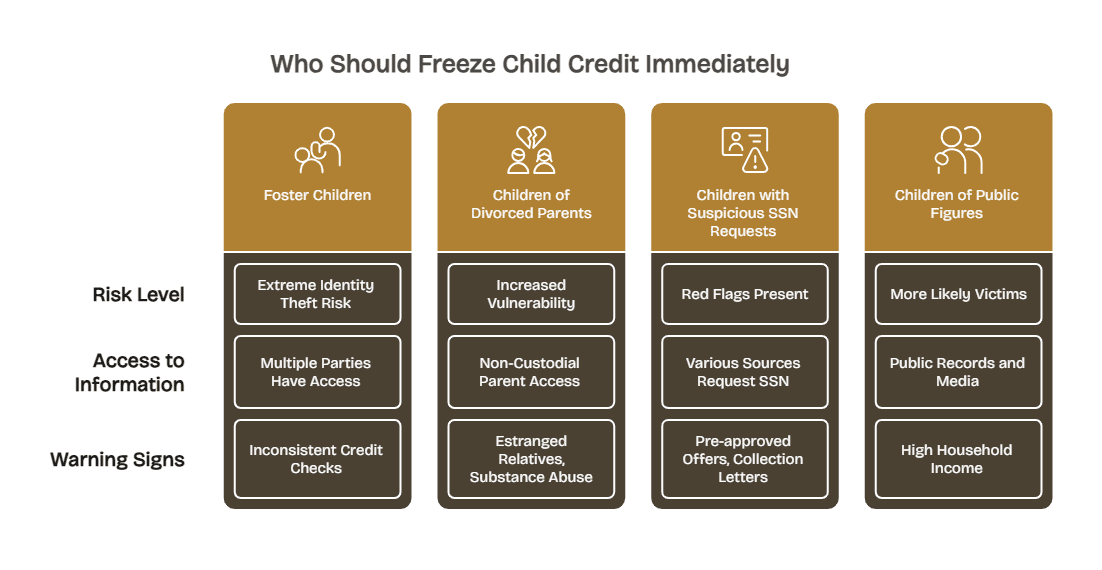

Who Should Freeze Child Credit Immediately

If any of the following applies to you, freezing your child’s credit immediately is a good idea.

Foster Children: Extreme Identity Theft Risk

Over half of children who should have received credit checks didn’t receive any in FY 2021, leaving them vulnerable. One study found that out of 96,000 foster children examined, more than 4,900 claimed someone used their Social Security numbers fraudulently.

Federal law requires annual credit checks for adolescents aged 14 or older in foster care, but compliance remains inconsistent. Foster parents, biological parents without custody, case workers, and administrative staff all have access to sensitive documents.

Children of Divorced Parents With Estranged Relatives

Contentious separations dramatically increase vulnerability. A non-custodial parent with access to birth certificates and Social Security cards can open credit accounts, utilities, or cell phone contracts – sometimes out of malice, often out of financial desperation.

Warning signs include: estranged relatives who previously had custody or document access, family members with substance abuse or gambling problems, relatives with poor credit or financial instability, and ongoing legal disputes over child support or custody.

Children With Suspicious SSN Requests

Red flags include: sports leagues requesting SSN without clear reason, online registrations asking for full SSN instead of last four digits, landlords requesting child SSN for adult accounts, and any government correspondence about employment or tax issues for a minor.

If your child receives pre-approved credit card offers before age 18, collection agency letters, IRS notices about unreported income, or denial letters for government benefits they never applied for – someone likely already used their identity.

Children of Public Figures and Wealthy Families

Children of families with $150,000+ yearly household income are more likely to be identity theft victims. Professional identity thieves research high-value targets whose names, birthdates, and personal information appear in news articles, social media, and public records.

Who Probably Doesn’t Need Child Credit Freeze

Here’s who can most likely avoid freezing their child’s credit.

Newborns in Stable Households

A newborn in a stable two-parent household with no estranged relatives, no custody disputes, and no unusual SSN requests faces minimal immediate risk. The SSN is fresh, known only to hospitals and the IRS.

Better Approach: Conduct annual credit checks and maintain strict document security. Revisit the freeze decision at age 10 when school participation increases exposure.

Children Under 10 With Clean Records

Elementary-age children in stable families who have never received suspicious communications face relatively low immediate risk. Focus on monitoring for early warning signs that would justify a freeze later.

Better Approach: Check for existing credit files annually and implement strong SSN protection. Only provide SSN when legally required. Consider parental control tools that monitor online activity.

When Monitoring Outperforms Freezes

Active monitoring through identity protection services like Aura detects suspicious activity and notifies you immediately. For moderate-risk families, paid monitoring may provide superior real-time protection.

Aura’s family plans monitor all three credit bureaus, scan dark web databases for exposed SSNs, and alert you to suspicious activity. The monitoring approach catches threats earlier than passive freezes.

The Freeze Process: What Actually Happens

Here’s what you need to know about freezing your child’s credit.

Why All Three Bureaus Must Be Frozen Separately

You must place a protected consumer freeze with each credit bureau individually, requiring written requests with supporting documentation. Freezing just one bureau leaves two others accessible to identity thieves.

Each bureau has different documentation requirements, mailing addresses, and processing times. This fragmentation is why many parents abandon the process halfway through.

| Bureau | Processing Time | Documentation | Mail Required |

| Experian | 3 business days | Online form + physical copies | Yes |

| Equifax | 5-10 business days | Paper form + birth certificate | Yes |

| TransUnion | 7-14 business days | Written letter + restrictive docs | Yes |

Documentation Requirements That Get Rejected

To place a freeze for minors, you must submit documentation proving authority to act on behalf of the minor including government-issued birth certificate, proof of your identity, and proof of the minor’s identity.

Common rejection reasons: photocopies instead of legible scans, birth certificates lacking official seals, proof of address documents older than 90 days, parent ID that doesn’t match current address, and missing signatures.

Timeline: 2-4 Weeks From Start to Completion

Adult credit freezes happen online in 60 seconds. After receiving your information, Experian will freeze the minor’s credit file within three business days, but you must mail physical documents first.

Realistic Timeline:

- Week 1-2: Gather and mail documents to three bureaus

- Week 3-4: Bureaus process and mail confirmations

- Week 5+: Follow up on missing confirmations or rejections

Better Alternatives for Low-Risk Families

In case freezing your child’s credit doesn’t seem like the right move, here are some alternatives to consider.

Annual Credit Report Checks for Children

Parents can request free credit reports for minor children by contacting credit bureaus directly. Annual checks reveal any existing credit files – which shouldn’t exist for minors – alerting you to identity theft before significant damage accumulates.

How to Request:

- Download forms from Experian, Equifax, and TransUnion websites

- Complete with your information and child’s information

- Include ID document copies proving parental authority

- Mail to bureau-specific addresses

- Receive reports within 30 days

If no credit file exists (normal for minors), the bureau confirms in writing. If a file exists, you’ve discovered theft early enough to dispute it.

Social Security Number Protection Best Practices

Identity thieves use Social Security numbers to fraudulently apply for credit cards, loans, and government benefits. Strong SSN protection prevents theft at the source.

Core Protection:

- Only provide SSN when legally required (taxes, school enrollment, medical care)

- Store birth certificates and Social Security cards in locked filing cabinets

- Never email SSNs or save in unencrypted files

- Review school privacy policies and request SSNs not be used as student IDs

- Limit digital footprint – don’t post birthdates on public social media

IRS Identity Protection PIN for Kids

The IRS Identity Protection PIN program provides six-digit codes that must be entered on tax returns, preventing fraudsters from filing false returns. In 2024, identity theft victims faced average losses of $1,600.

Parents can request IP PINs for dependent children if they’ve been victims or want proactive protection. The IP PIN changes annually and blocks thieves from filing false returns.

School SSN Request Policies

Schools house valuable information for bad actors, making them top targets. Federal law (FERPA) protects student records but doesn’t prohibit SSN collection. Many parents don’t realize they can decline non-mandatory SSN requests.

Questions to Ask:

- Is this SSN request legally mandatory or optional?

- What specific purpose will the SSN serve?

- How is the SSN stored and who has access?

- Can an alternative identifier be used instead?

If Your Child Already Has a Credit File

Immediate Emergency Response

If you suspect identity theft, TransUnion can check their database for a credit file with your child’s Social Security number and guide you through next steps.

First 24 Hours:

- Request credit reports from all three bureaus

- Review for fraudulent accounts, credit cards, loans

- Document everything with photos and notes

- Place fraud alerts on child’s credit file

- File identity theft report at IdentityTheft.gov

First Week:

- Contact every creditor listed on fraudulent accounts

- Notify them accounts were opened fraudulently

- Request written confirmation of closures

- File police report (required for some disputes)

- Send dispute letters to all three bureaus

Why Recovery Takes 6-12 Months

Adult identity theft victims resolve issues quickly because they have established credit histories. Children’s cases require extensive documentation proving minors couldn’t legally enter credit agreements.

Recovery Timeline Factors:

- Legal documentation proving age and incapacity

- Multiple separate creditor disputes

- Police investigation delays (especially with family members)

- 30-45 day bureau investigation periods

- Verification loops requiring multiple follow-ups

Consider professional assistance through Identity Guard that provides dedicated case managers for recovery coordination.

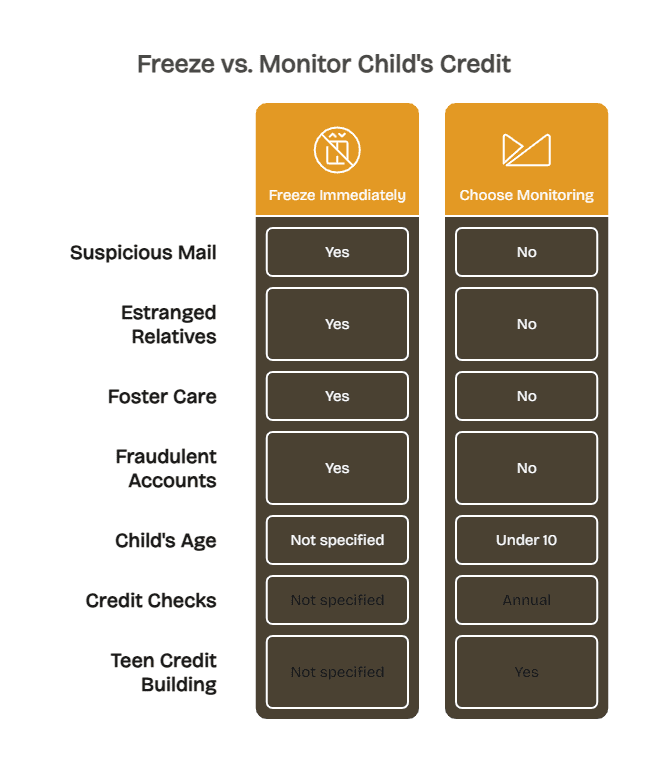

When to Freeze vs. Monitor

Freeze Immediately If:

- Child received suspicious mail or correspondence

- Estranged relatives had document access

- Child entering or in foster care

- Discovered existing fraudulent accounts

Choose Monitoring If:

- Child under 10 with zero suspicious activity

- No custody disputes or estranged relatives

- Can commit to annual credit checks

- Want flexibility for teen credit building

Consider Bark parental controls for monitoring online activity alongside Aura family identity protection for comprehensive coverage.

Recommended Monitoring Services

| Service | Key Feature | Best For | Price |

| Aura | Unlimited child monitoring + parental controls | All-in-one family protection | $8-32/month |

| Identity Guard | Dark web monitoring + credit alerts | Breach detection priority | $7-25/month |

| Bark | Social media monitoring across 30+ platforms | Active teen social media users | $14/month |

Making the Right Choice

Credit freezes aren’t universal solutions. Your decision depends on risk factors: foster care status, estranged relatives, suspicious SSN requests, public figure exposure, and existing signs of misuse.

High-risk families should freeze immediately. Low-risk families achieve better protection through annual monitoring, strong SSN protection, and active vigilance. Understanding dark web dangers helps contextualize the broader threat landscape facing families.

The key insight: protection strategies should match actual threats, not hypothetical worst-case scenarios. Tailor your approach to your situation, revisit every 2-3 years, and stay alert for warning signs.

Protect your family’s identities with comprehensive monitoring – explore Batten’s identity protection collection for services that detect suspicious activity before it becomes a financial disaster, including Cloaked digital footprint protection for families.

Frequently Asked Questions

Does Freezing My Child’s Credit Affect Their Future Credit Score?

No, credit freezes have zero impact on credit scores because they don’t appear on credit reports. When your child becomes an adult and lifts the freeze, they start with a clean slate – no credit history but also no negative marks. The freeze prevents unauthorized accounts during childhood without damaging future creditworthiness.

Can I Freeze My Child’s Credit Online Like My Own?

No, minor credit freezes require physical mail with extensive documentation proving parental authority. Parents must mail requests with documentation to Equifax, Experian, and TransUnion separately. This process takes 2-4 weeks versus instant online freezes for adults over 18.

What Happens to the Freeze When My Child Turns 18?

If not removed, the freeze remains as a protected consumer freeze. Once they turn 18, your child can convert it to a standard credit freeze and manage it through online accounts at each credit bureau instead of requiring parental involvement.

How Do I Know If Someone Already Opened Accounts in My Child’s Name?

Request free credit reports from all three bureaus using the annual credit check process. If any credit file exists (which shouldn’t happen), it indicates identity theft. Watch for warning signs: credit card offers, collection notices, IRS letters about unreported income, or benefit letters in your child’s name.

Will a Credit Freeze Prevent My Ex-Spouse From Misusing My Child’s Identity?

Credit freezes block new credit applications but don’t prevent employment fraud, medical identity theft, or tax fraud. In 75% of child identity theft cases, the perpetrator is someone the child knows like a parent or relative. For family member threats, combine freezes with monitoring services like Norton LifeLock and consider legal protection orders.

Can My Teenager Build Credit With a Frozen Credit Report?

Yes, but you must unfreeze their credit first before authorized user additions, secured credit cards, or student credit cards. Many parents forget about childhood freezes and discover the block only when teen applications are denied. Proactively unfreeze at age 16-17 when building credit history.

Does Credit Monitoring Replace the Need for a Child Credit Freeze?

Credit monitoring and freezes serve different purposes – monitoring detects misuse with immediate alerts while freezes prevent unauthorized account openings. For high-risk children, use both. For moderate to low-risk families, comprehensive monitoring services like Aura may provide adequate protection with greater flexibility than static freezes.

How Long Does It Take to Unfreeze My Child’s Credit?

Unfreezing requires the same mail-based process as freezing – submitting written requests with documentation to all three bureaus. Expect 2-4 weeks for complete unfreezing. Plan ahead for college applications, apartment rentals, or authorized user additions that require credit verification.

What’s the Difference Between a Credit Freeze and Fraud Alert?

A credit freeze blocks all access to credit reports, preventing new account openings. A fraud alert requires creditors to verify identity before granting credit but doesn’t prevent access to reports. For children, freezes provide stronger protection, but fraud alerts work well as temporary measures or alongside monitoring services.

Can Foster Parents Freeze a Foster Child’s Credit?

Yes, federal law requires child welfare agencies to conduct annual credit checks for foster youth aged 14+, and foster parents or agency representatives can request credit freezes. State requirements vary, but most allow authorized representatives to freeze credit on behalf of minors in their care.

Is a Child Credit Freeze Worth It for Newborns?

For newborns in stable families with no risk factors, annual monitoring may be more practical than immediate freezes. The newborn credit freeze worth it question depends on your risk profile. If you have estranged relatives, custody concerns, or public exposure, freeze immediately. Otherwise, implement strong SSN protection and annual checks.

Sources

- Child Identity Fraud: A Web of Deception and Loss. 2021. Javelin Strategy & Research (Escalent). https://javelinstrategy.com/sites/default/files/files/reports/21-5012J-FM-2021%20Child%20Identity%20Fraud%20Study_1.pdf

- Credit Freezes and Fraud Alerts. 2025. Federal Trade Commission. https://consumer.ftc.gov/articles/credit-freezes-and-fraud-alertsHow Identity Theft Impacts Children. 2026. Internet Matters. https://www.internetmatters.org/issues/privacy-identity/learn-about-privacy-and-identity-theft/

- One in Every Fifty Children Falls Victim to Identity Theft Each Year. 2025. London Stock Exchange Group (LSEG) Risk Intelligence. https://www.lseg.com/en/media-centre/press-releases/2025/one-in-every-fifty-children-falls-victim-to-identity-theft-each-year

- Most Worrying Identity Theft Statistics for 2026. 2024. Fortunly. https://fortunly.com/statistics/identity-theft-statistics/

- Child Identity Theft. 2026. TransUnion. https://www.transunion.com/fraud-victim-resources/child-identity-theft

- Why Parents May Want to Start Locking a Child’s Credit at a Very Young Age. 2024. CNBC. https://www.cnbc.com/2024/08/23/identity-theft-of-americas-youngest-generation-is-on-the-rise.html

- 25 Percent of Kids Will Face Identity Theft Before Turning 18. Age-Verification Laws Will Make This Worse. 2024. R Street Institute. https://www.rstreet.org/commentary/25-percent-of-kids-will-face-identity-theft-before-turning-18-age-verification-laws-will-make-this-worse/

- Freezing Your Child’s Credit Report: FAQ. 2026. Equifax. https://www.equifax.com/personal/education/identity-theft/articles/-/learn/freezing-your-childs-credit-report-faq/

- Should You Freeze Your Child’s Credit File? 2024. Experian. https://www.experian.com/blogs/ask-experian/should-you-freeze-your-childs-credit-file/

- Most Children in Foster Care Did Not Receive Credit Checks and Assistance. 2024. U.S. Department of Health and Human Services Office of Inspector General. https://oig.hhs.gov/reports/all/2024/most-children-in-foster-care-did-not-receive-credit-checks-and-assistance/